Logistic Regression From Scratch: Predicting a Win, Not a Number

What you'll build

A pure-numpy logistic regression that predicts whether the home team wins from the net-rating gap, learned with the same gradient descent from tutorial 70 - reaching 67% accuracy against a 54% baseline.

In the gradient-descent tutorial we taught a model to fit a straight line by stepping downhill on its error. A line is the right shape for predicting a number — wins, points, run differential. But plenty of the questions we actually care about are yes/no: did the home team win? A straight line answers that badly — it happily predicts a "probability" of 1.4 or −0.2, which is nonsense. Logistic regression fixes it with one small change: squash the line through a sigmoid so the output is always a real probability between 0 and 1, then learn the weights with the exact same downhill steps.

We'll build it from scratch in pure numpy to predict the NBA home win from a single feature — the gap in season net rating between the two teams. The data is bundled (nba_ratings.csv and nba_home_results.csv, 1,231 real games), so it runs offline.

Go deeper with the free textbook: Chapter 27: Logistic Regression and Classification at DataField.dev.

-

Build the dataset: a gap, and a yes/no

The feature is how much better the home team is by season net rating; the label is whether it won. We standardize the feature to a z-score so a single learning rate behaves — the same habit from gradient descent.

python import numpy as np, pandas as pd ratings = pd.read_csv("nba_ratings.csv") nrtg = dict(zip(ratings.Team, ratings.NRtg)) g = pd.read_csv("nba_home_results.csv") g["gap"] = g.home_team.map(nrtg) - g.away_team.map(nrtg) # home edge g["home_win"] = (g.home_pts > g.away_pts).astype(int) # the target x = ((g.gap - g.gap.mean()) / g.gap.std()).to_numpy() y = g.home_win.to_numpy().astype(float)What we're predictingGames: 1231 Home teams won 54.3% of them (the baseline to beat). Net-rating gap ranges from -22.3 to 22.3 points.

Home teams win 54.3% of the time — that's the baseline any model has to beat. Always guessing "home wins" is right 54.3% of the time; if our model can't do better, it's learned nothing.

-

The sigmoid: a line that can't escape 0 and 1

The whole trick is one function. Take the linear score

z = w·x + b— which can be any number from −∞ to +∞ — and pass it through the sigmoid. Big positivez→ near 1; big negative → near 0;z = 0→ exactly 0.5. Now the output is always a valid probability.python def sigmoid(z): return 1.0 / (1.0 + np.exp(-z))That S-shape is the entire difference between linear and logistic regression. Everything else — the gradient descent, the loss curve — is the same machinery you already built.

-

The right loss for a probability: log-loss

Mean squared error is the wrong tool here; for classification we use log-loss (cross-entropy), which punishes confident wrong answers hard and rewards confident right ones. The beautiful part: when you predict with a sigmoid and score with log-loss, the gradient simplifies to exactly the same form as before —

(prediction − truth)times the input.python w, b = 0.0, 0.0 lr = 0.3 losses = [] for step in range(400): p = sigmoid(w * x + b) # predicted probabilities losses.append(-np.mean(y*np.log(p+1e-12) + (1-y)*np.log(1-p+1e-12))) err = p - y # same gradient shape as linear! w -= lr * np.mean(err * x) b -= lr * np.mean(err)Predict, measure the error, step downhill, repeat — the identical skeleton from gradient descent. Only the prediction function (sigmoid) and the loss (log-loss) changed.

-

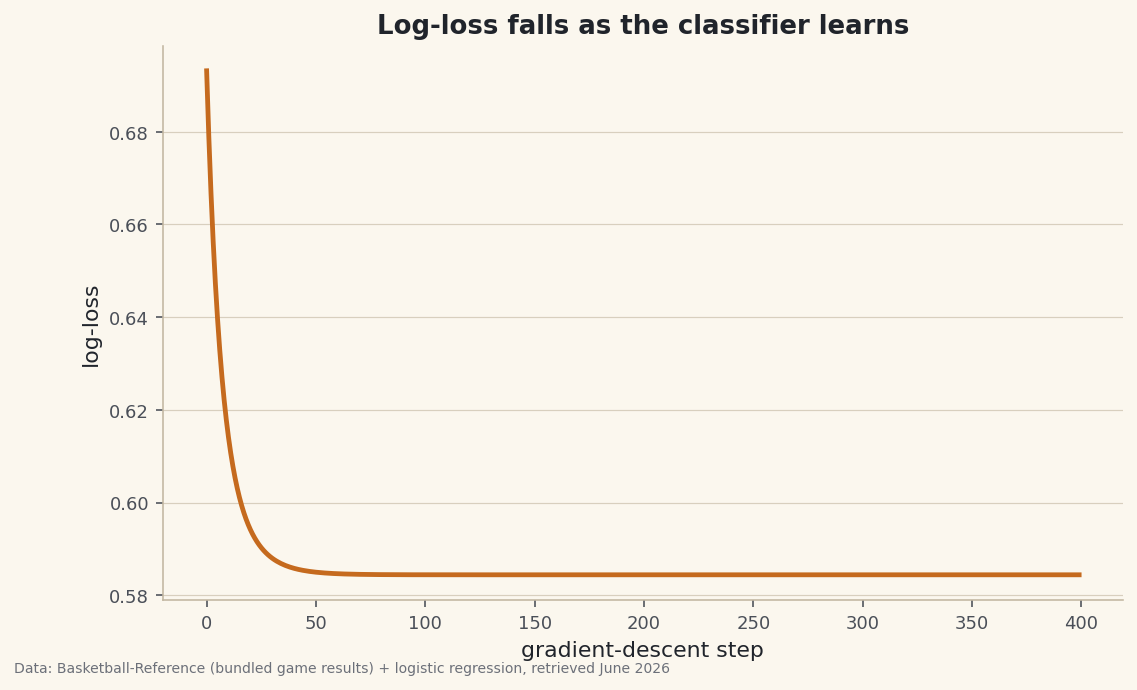

Watch the log-loss fall

Same diagnostic as always: plot the loss against the training step. A healthy run drops fast then flattens.

python import matplotlib.pyplot as plt fig, ax = plt.subplots() ax.plot(losses) ax.set_xlabel("step"); ax.set_ylabel("log-loss") fig.savefig("logit_loss.png", dpi=144, bbox_inches="tight")

Data: Bundled Basketball-Reference net ratings + 1,231 game results + logistic regression, retrieved June 2026 It starts at 0.693 — that's the log-loss of a coin flip, the model knowing nothing — and settles near 0.584. The drop is the model learning that a bigger net-rating gap means a more likely home win.

-

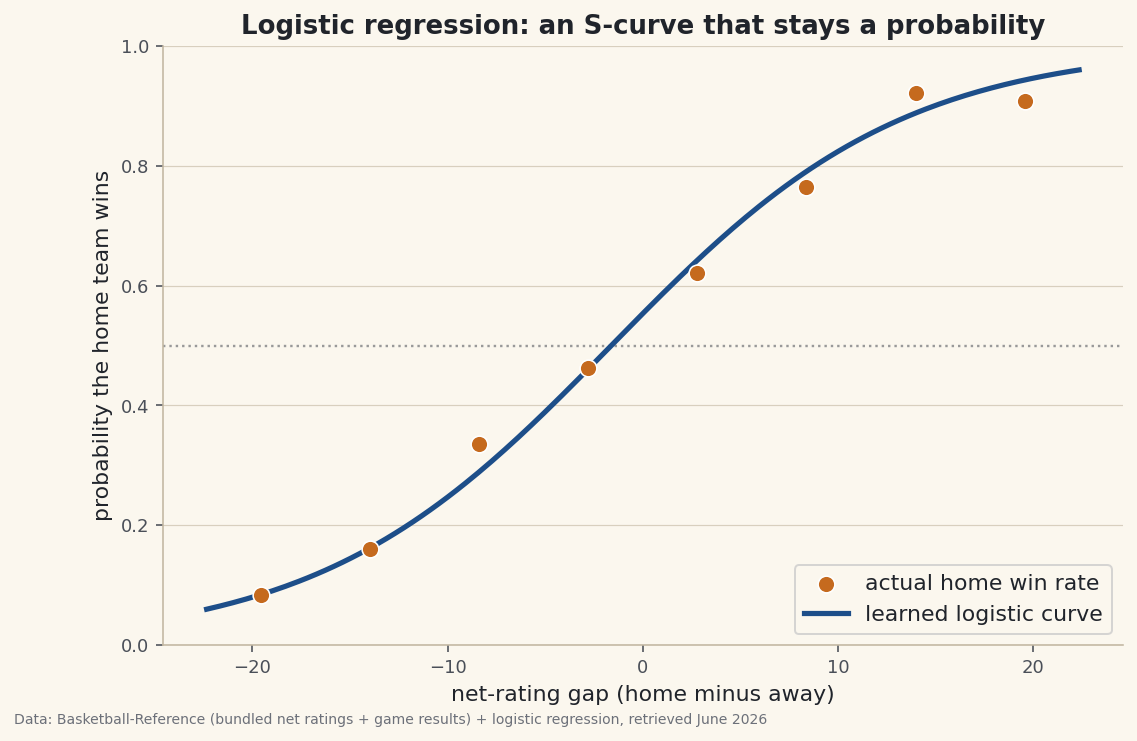

See the S-curve trace the real win rates

Now plot the learned curve over the data. Bucket the games by net-rating gap and mark each bucket's actual home win rate; the logistic curve should thread right through them.

python fig, ax = plt.subplots() gx = np.linspace(g.gap.min(), g.gap.max(), 200) gz = (gx - g.gap.mean()) / g.gap.std() ax.plot(gx, sigmoid(w * gz + b)) # the learned probability curve ax.set_ylim(0, 1) fig.savefig("logit_curve.png", dpi=144, bbox_inches="tight")Data: Bundled Basketball-Reference net ratings + 1,231 game results + logistic regression, retrieved June 2026 The dots are reality; the curve is the model. When the home team is much worse (a gap of −20) it wins only about a fifth of the time; when it's much better (+20) it wins over 80%. At a gap of zero the curve sits just above 0.5 — the residual home-court edge after talent is equal.

-

How good is it? Beat the baseline

Turn probabilities into yes/no by thresholding at 0.5, then check accuracy against the truth.

python acc = ((sigmoid(w*x + b) >= 0.5) == y).mean()The trained classifierStart log-loss: 0.6931 After 400 steps: 0.5844 Learned weight w = 1.064, intercept b = 0.217 Accuracy: 67.3% (vs 54.3% from always guessing 'home wins') A home team +6 in net rating is predicted to win 73% of the time.

The model is right 67.3% of the time — a real 13-point lift over the 54.3% you'd get from always guessing "home wins." And it's interpretable: a home team six net-rating points better than its opponent is predicted to win about 73% of the time. One feature, one S-curve, and you've got a calibrated win-probability model.

Troubleshooting

I get RuntimeWarning: overflow in exp

For very large negative z, np.exp(-z) overflows. It's harmless here because the result just saturates to 0, but to silence it cleanly use the numerically stable form np.where(z >= 0, 1/(1+np.exp(-z)), e/(1+e)) with e = np.exp(z), or clip z to a sane range before the sigmoid.

My accuracy is stuck at 54%

That's the baseline — the model is predicting "home wins" for everyone. Usually the learning rate is too small or you ran too few steps, so the weight never moved. Check that the log-loss is actually falling; if it's flat, raise lr or add steps. Also confirm you standardized the feature.

Why log-loss instead of accuracy as the loss?

Accuracy is a step function — it doesn't change as you nudge the weights slightly, so it has no useful gradient to descend. Log-loss is smooth and rewards being confidently right, which gives gradient descent something to follow. We optimize log-loss and report accuracy.

Challenge yourself

Add a second feature — rest days, or back-to-backs — and watch the gradient gain one more component while the loop stays identical. Then split the games into train and test sets and measure accuracy on games the model never saw, the honest way to grade a classifier (see Chapter 29: Evaluating Models). Finally, plot a calibration curve: bin your predicted probabilities and check that games you called "70%" really won about 70% of the time.

Get the code

Here's the complete, working script for this tutorial. It runs exactly as shown.

Download the finished script (71_logistic_regression_from_scratch.py)This script imports a small shared helper (and reads any bundled sample data) that live next to it in /downloads/ — grab these into the same folder so it runs as-is: sdt_common.py, sdt_nba.py.